연준의 리세션 체크 포인트, 단기 포워드 스프레드

FRED self-caculation ver

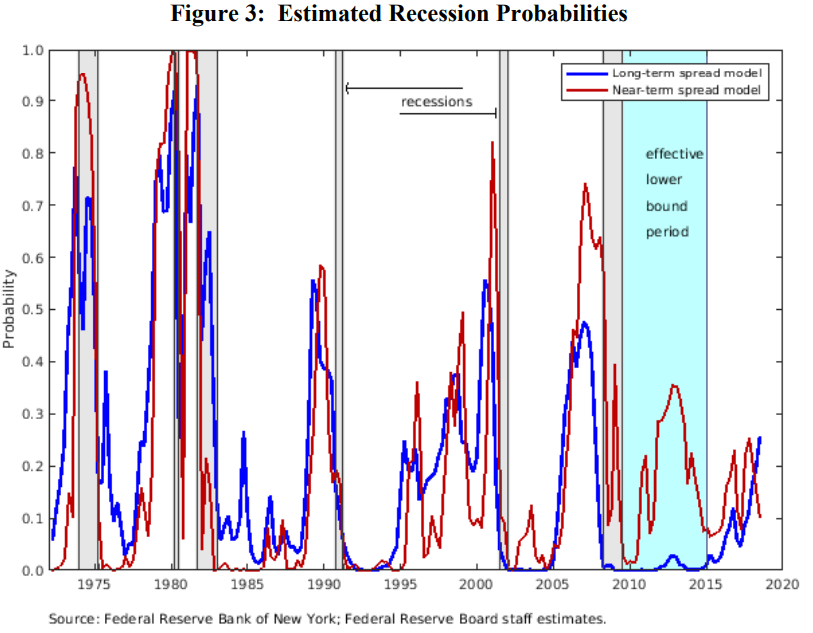

FRED로 계산한 '단기 포워드 스프레드(Near-term forward yield spread)'입니다. 일반적으로 10y-2y 등 장단기 금리차는 미국 경제의 리세션을 전망할 때 금융시장이 가장 많이 참고하는 지표 중 하나입니다.

여기서 소개하는 단기 포워드 스프레드란 미국 국채 3개월물의 18개월 후 선도금리에서 3개월물 금리를 빼준 것을 말합니다(18M3M forward – 3M spot). 실제로 연준은 10y-2y 스프레드 보다는 단기 포워드 스프레드를 더욱 살피는 것으로 알려져 있습니다. 파월의 발언에서도 여러 차례 등장한 바 있는 지표죠. 파월 의장은 ‘21년 3월 21일 전미실물경제협회(NABE) 연례 커퍼런스에서 리세션과 관련해 장단기 스프레드보다는 단기 포워드 스프레드가 보다 더 정확한 설명력을 가지고 있다고 강조한 바 있습니다. 또한 연준은 '22년 3월 <(Don’t Fear) The Yield Curve, Reprise>라는 FED Note를 게시하며 10y-2y 스프레드 역전을 우려하는 이들의 불안감을 다소 덜어낸 바 있습니다(아래 링크 참조).

연준 이코노미스트 에릭 엥스트롬과 스티븐 샤프가 '18년 6월에 발표한 논문 <The Near-Term Forward Yield Spread as a Leading Indicator: A Less Distorted Mirror>을 보면 더 상세한 정보를 얻으실 수 있습니다(아래 링크 참조). 해당 논문을 보면, 연준은 (3개월물의 18개월 후 선도금리에서 3개월물 금리를 빼준) 단기 포워드 스프레드가 장단기 금리차 보다 "12~18개월 내 임박한 리세션"을 더욱 잘 예측해낸다고 설명합니다. 18개월 후 선도금리가 역전된다면 현재 3개월물의 금리가 과도하게 타이트함을 의미합니다. 일각에선 이를 통화정책 여력으로 해석하기도 합니다.

FRED에서 계산한 단기 포워드 스프레드는 이코노미21의 양 기자님의 계산을 참고하였으며, 양 기자님은 현재 이코노미21에서 연준와처라는 이름으로 연준의 행보를 밀접하게 관찰하고 계십니다. 연준의 정책이나 순유동성 관점에서 자주 읽어보는 컨텐츠이니 일독을 권합니다.

연준의 금리 인상 주기가 끝을 향해 달려가는 지금 해당 지표의 중요성은 보다 더 부각될 것으로 보입니다.

관련 링크 올려드립니다.

(Don't Fear) The Yield Curve, Reprise

March 25, 2022 (Don't Fear) The Yield Curve, Reprise Eric C. Engstrom and Steven A. Sharpe1 Introduction In recent months, financial market perceptions about the future path of short-term interest rates have evolved amidst signals from policymakers suggest

www.federalreserve.gov

The Fed - The Near-Term Forward Yield Spread as a Leading Indicator: A Less Distorted Mirror

August 2018 (Revised March 2019) The Near-Term Forward Yield Spread as a Leading Indicator: A Less Distorted Mirror Eric C. Engstrom, Steven A. Sharpe Abstract: The spread between the yield on a 10-year Treasury note and the yield on a shorter maturity sec

www.federalreserve.gov

NTFS ver

아래 첨부한 사이트 역시 단기 포워드 스프레드를 다루고 있는데, 두 계산법 간 차이는 그리 크지 않다고 생각됩니다. 보기에는 요게 더 깔끔할 수 있겠네요.

https://www.neartermforwardspread.com/

Near Term Forward Spread

Near Term Forward Spread Data Anthony Diercks & Daniel Soques This chart shows the up-to-date calculation of the near term forward spread (NTFS) as outlined by Engstrom and Sharpe (2019) using U.S. yield curve data from the Federal Reserve Board of Governo

www.neartermforwardspread.com

'Article Archives' 카테고리의 다른 글

| 시장 참여자들은 금리 기대 조정에 적응 중 (0) | 2023.07.18 |

|---|---|

| 견고한 하이일드·Fallen Angels 채권 (0) | 2023.07.17 |

| 7월부터 반등하는 인플레이션? (0) | 2023.07.16 |

| 기대 인플레이션 예상치 상회 (0) | 2023.07.15 |

| 워렌 버핏 미국 LNG 터미널 지분 50% 인수 (0) | 2023.07.14 |